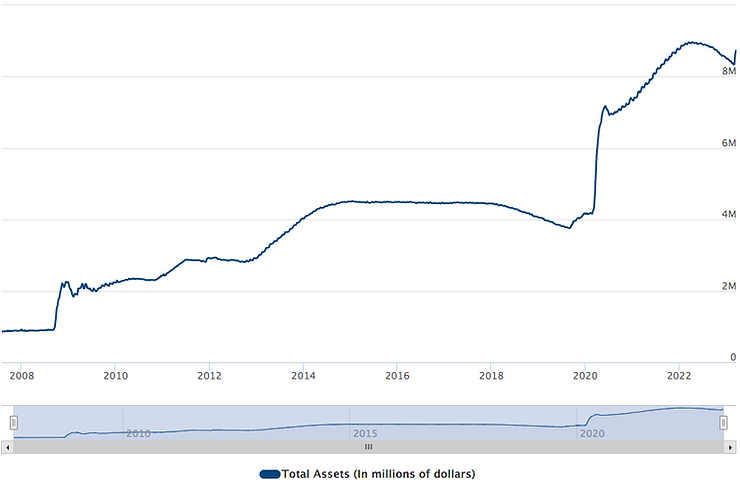

We are simple, logical thinkers here at Warcap, which may be boring at times. But our process is reliable, especially in times of chaos. One of the most basic macro indicators we follow in the Fed balance sheet. Remarkably, the Fed began Quantitative Easing (QE) again by lending $460 billion to banks through the Discount Window and the Bank Lending Program in the past two weeks. That is a huge number as noted in this chart.

The bankers I know tell me that they simply want to flood the system with cash to quell any public liquidity concerns. But isn’t that exactly the purpose of the discount window? What I do know is that banks that borrow from the discount window have a poor performance history thereafter. What is also concerning is that the Fed is lending the treasuries the banks pledge at PAR, far above the current market value of those securities. This is yet another phantom program that will mask the true hole in the bank’s balance sheets. In my opinion, the solution is to simply reinstate the 10% reserve requirement that was eased during covid, which no one seems to be discussing. Having 10% of the deposits in the system would be soothing right now. Regardless, our job is to implement investments during all periods, and quantitative easing has us intrigued.

Tracking the Fed balance sheet versus the stock market is a helpful exercise and the correlation is clear. The Fed digitally creates cash and then deploys it by purchasing securities, like mortgages and treasuries. When the economy and markets are operating smoothly, which is becoming increasingly rare, there is no need for Fed support. During contagions, like housing in 2008 or Covid, the Fed can go into hyperdrive and flood the system with new digitally minted cash through security purchases. Covid support was extreme as the Fed doubled its balance sheet to $9 trillion. Inflation was bound to follow and the remedy has been to increase rates and reduce the balance sheet, until this month.

This new QE is an inflection point and we probably have reached the peak in interest rates during this cycle. Rates will likely stay in this current 4% range for some time and interest-bearing securities like short-term treasuries will continue to attract capital. Investors looking to deploy capital as well as companies looking to receive that capital need to adjust to this new reality. Run your business to earn multiples of the treasury bills or don’t expect to receive a capital allocation. There are many businesses that do, and we are focused on them.

Warren Capital Group’s foundational planning software allows you to access your online financial information in one place so you can easily monitor your portfolio, including investment, retirement, and credit card accounts.

There are multiple aspects to managing wealth and they require a consistent, disciplined approach. Our wealth management practice has discipline at its core and is designed to help our clients grow and protect their net worth.

Give your employees a benefit plan that will allow them to begin saving for retirement. We sit down with each company and assess the benefits of each type of plan for both the company and their employees. Employees will also have access to our foundational planning software.

For any inquiries, questions or commendations, please call: 854-246-8881 or fill out the following form

© 2026 Warren Capital Group. All Rights Reserved.