For the first time in 15 years, the bond market is offering “real return”, which subtracts taxes and inflation from interest. With treasury notes paying 5.5% and CPI at 3%, bond yields are attractive, and we’ve added treasuries to client portfolios. Higher rates warrant investment, which also creates a headwind for equities as money is now flowing out of various areas of the stock market. But capital will also flow to the asset offering the most yield with the least risk. Because it’s been so long since debt has been a viable investment, investors still haven’t fully adjusted to this new rate reality, and we are taking notice. But this capital allocation isn’t the only challenge for equities right now as the Fed’s balance sheet is shrinking.

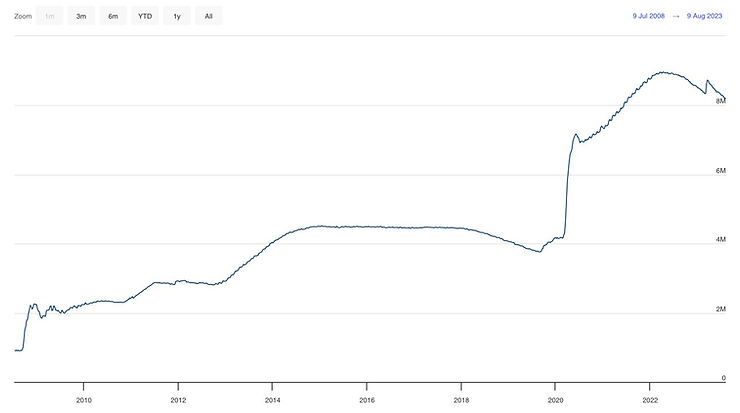

The Federal Reserve tool that catches the most headlines is the Fed funds rate, which the Fed adjusts to control monetary policy and to reign inflation. However, they have another lever just as effective and it’s their balance sheet. When the Fed wants to stimulate growth they create new dollars, which then must be deployed through asset purchases of treasuries and mortgages. This transaction is reflected in their balance sheet, which doubled during covid. Of recent, the balance sheet has been shrinking, and the decrease

in money supply simply means there are fewer dollars in circulation to support asset prices. This is a significant challenge for all assets and the riskiest fall first. This doesn’t mean that certain stocks and bonds can’t perform, but it is another headwind that can’t be ignored. An allocation of stocks and bonds is appropriate now and security selection is critical. This is the ideal environment for an active investment manager and our clients are enjoying the benefits.

As always, I appreciate your continued trust and confidence.

Warren Capital Group’s foundational planning software allows you to access your online financial information in one place so you can easily monitor your portfolio, including investment, retirement, and credit card accounts.

There are multiple aspects to managing wealth and they require a consistent, disciplined approach. Our wealth management practice has discipline at its core and is designed to help our clients grow and protect their net worth.

Give your employees a benefit plan that will allow them to begin saving for retirement. We sit down with each company and assess the benefits of each type of plan for both the company and their employees. Employees will also have access to our foundational planning software.

For any inquiries, questions or commendations, please call: 854-246-8881 or fill out the following form

© 2026 Warren Capital Group. All Rights Reserved.